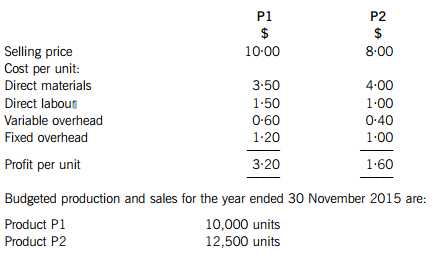

The following scenario relates to questions 6–10.Corfe Co is a business which manufactures

The following scenario relates to questions 6–10.

Corfe Co is a business which manufactures computer laptop batteries and it has developed a new battery which has a longer usage time than batteries currently available in laptops. The selling price of the battery is forecast to be $45.

The maximum production capacity of Corfe Co is 262,500 units. The company’s management accountant is currently preparing an annual flexible budget and has collected the following information so far:

In addition to the above costs, the management accountant estimates that for each increment of 50,000 units produced, one supervisor will need to be employed. A supervisor’s annual salary is $35,000.

The production manager does not understand why the flexible budgets have been produced as he has always used a fixed budget previously

Assuming the budgeted figures are correct, what would the flexed total production cost be if production is 80% of maximum capacity?

A.$2,735,000

B.$2,770,000

C.$2,885,000

D.$2,920,000

In the first month of production of the new battery, actual sales were 18,000 units and the sales revenue achieved was $702,000. The budgeted sales units were 17,300.

Based on this information, which of the following statements is true?

A.When the budget is flexed, the sales variance will include both the sales volume and sales price variances

B.When the budget is flexed, the sales variance will only include the sales volume variance

C.When the budget is flexed, the sales variance will only include the sales price variance

D.When the budget is flexed, the sales variance will include the sales mix and quantity variances and the sales price variance

Which of the following statements relating to the preparation of a flexible budget for the new battery are true?

(1) The budget could be time-consuming to produce as splitting out semi-variable costs may not be straightforward

(2) The range of output over which assumptions about how costs will behave could be difficult to determine

(3) The flexible budget will give managers more opportunity to include budgetary slack than a fixed budget

(4) The budget will encourage all activities and their value to the organisation to be reviewed and assessed

A.1 and 2 only

B.1, 2 and 3

C.1 and 4

D.2, 3 and 4

The management accountant intends to use a spreadsheet for the flexible budget in order to analyse performance of the new battery.

Which of the following statements are benefits regarding the use of spreadsheets for budgeting?

(1) The user can change input variables and a new version of the budget can be quickly produced

(2) Errors in a formula can be easily traced and data can be difficult to corrupt in a spreadsheet

(3) A spreadsheet can take account of qualitative factors to allow decisions to be fully evaluated

(4) Managers can carry out sensitivity analysis more easily on a budget model which is held in a spreadsheet

A.1, 3 and 4

B.1, 2 and 4

C.1 and 4 only

D.2 and 3

The management accountant has said that a machine maintenance cost was not included in the flexible budget but needs to be taken into account.

The new battery will be manufactured on a machine currently owned by Corfe Co which was previously used for a product which has now been discontinued. The management accountant estimates that every 1,000 units will take 14 hours to produce. The annual machine hours and maintenance costs for the machine for the last four years have been as follows:

What is the estimated maintenance cost if production of the battery is 80% of maximum capacity (to the nearest $’000)?

A.$575,000

B.$593,000

C.$500,000

D.$735,000

请帮忙给出每个问题的正确答案和分析,谢谢!

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

如果结果不匹配,请 联系老师 获取答案

如果结果不匹配,请 联系老师 获取答案

更多“The units of production deprec…”相关的问题

更多“The units of production deprec…”相关的问题